While you’ve likely heard about these tax-efficient savings accounts, what exactly is an ISA and which is best for you? In this article, we explain ISAs, how they work and the types available. We’ll cover the ISA allowances, deadlines and rules before summing up with an ISA comparison so you can find the very best ISA this year.

What is an ISA and how does it work?

So, what does ISA stand for? This is an abbreviation of Individual Savings Account. ISAs are tax-free savings or investment accounts which are available to UK residents. This means, unlike non-ISA investments, you can save or invest your money in an ISA without paying tax on the resultant interest, dividend income or capital gains. While the tax benefits are obvious, you also have the ability to choose between multiple types of ISAs. This has made them an exceptionally popular choice amongst UK investors and savers.

What ISA types are available?

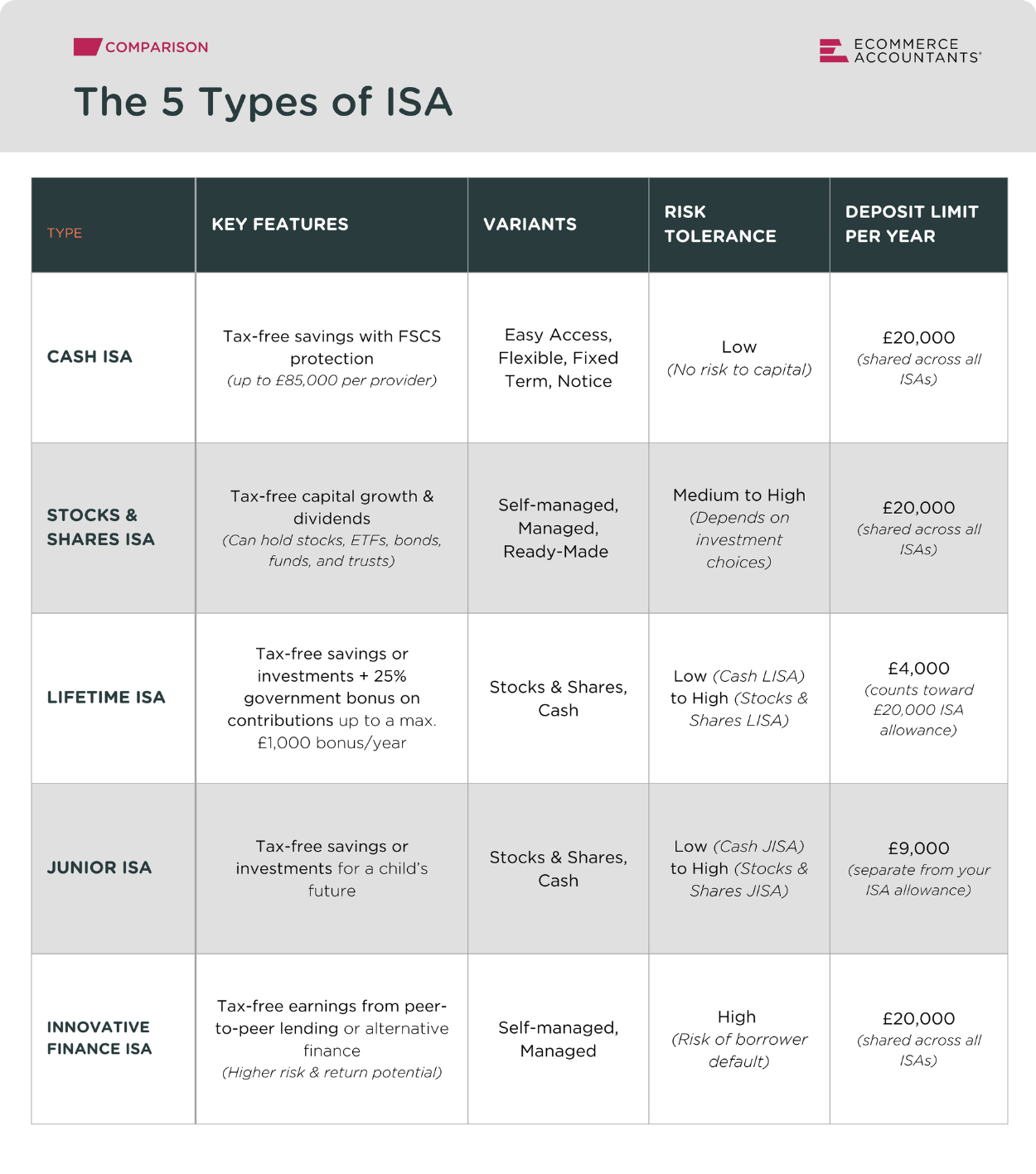

There are 5 main types of ISA available in the UK. You are only allowed to open 1 of each type of ISA per tax year.

Depending on your preference, you might choose to open a:

- Cash ISA – This is the simplest form of ISA and works just like a savings account, the difference being that any interest you accrue is tax-free.

- Stocks and Shares ISA – This type of ISA allows you to invest in stocks, funds and more (depending on provider). Compared to a general investment account, the downside is that the pool of available investments is slightly more restricted, for example you can’t directly hold commodities or cryptocurrencies in an ISA. The upside is that any growth (capital gains) or dividend income is completely tax-free.

- Lifetime ISA – Often referred to as a LISA, this type is only available to those between the ages of 18 and 39. This ISA allows you to earn an attractive 25% government bonus on your savings each year. The maximum you can contribute is £4,000 per year (where your bonus would be £1,000). To avoid penalties, you can only withdraw your LISA investment to either purchase your first home (up to £450,000 with a mortgage) or for retirement (after the age of 60).

- Junior ISA – Often shortened to JISA, this is designed for children under the age of 18 in the UK. As a parent or guardian, you can save or invest funds on behalf of a child. There are 2 types, a Junior Stocks & Shares ISA and a Junior Cash ISA. Any interest, dividend income or capital gains are tax-free. The money belongs to the child although it is locked until they turn 18 years old. As a parent/guardian, you are allowed to open 1 of each type of JISA per child per tax year.

- Innovative Finance ISA – An IFISA allows you to lend your funds to individuals or businesses through approved peer-to-peer lending or crowdfunding platforms. As with any form of lending, you may earn interest but with an IFISA, that interest will be tax-free.

If you wish to compare the top accounts currently available, see our comparisons of the best Stocks and Shares ISAs, Cash ISAs, Junior ISAs and best Lifetime ISAs.

ISA Allowance 2024/2025

What is the ISA Allowance? This represents the maximum amount of money you can save or invest within an ISA each year while keeping it tax-free. This personal ISA limit is set by the government and resets each tax year on the 6th of April.

The annual ISA allowance for 2024/2025 is £20,000 per person. While your total contributions into ISAs cannot exceed £20,000, you can split this amount across multiple types of ISAs. This means you could, for example, invest £10,000 in a Stocks and Shares ISA, £4,000 in a Lifetime ISA and £6,000 in a Cash ISA.

If you plan to apportion your £20,000 into multiple types, then consider the ISA-specific annual limits. This is the maximum you could apportion to each type of ISA in a tax year:

- Lifetime ISA Allowance - £4,000

- Cash ISA Allowance - £20,000

- Stocks and Shares ISA Allowance - £20,000

- Innovative Finance ISA Allowance - £20,000

The Junior ISA Allowance is £9,000 per child. This applies across all Junior ISA types (you may open a Junior Cash ISA and a Junior Stocks & Shares ISA for one child). It’s important to note that contributions you make to your child’s JISA do not affect your own personal ISA allowance. For example, you could fund your personal ISAs up to £20,000 and, separately, you could also fund your child’s JISA/s up to £9,000 in any given year.

ISA Deadline 2024/2025

This tax free ISA allowance of £20,000 resets each year on the 6th of April. This means the deadline for contributing funds into your ISA/s is midnight on the 5th of April 2025 for the 2024/2025 tax year. After the deadline, any of your unused ISA allowance is lost, meaning you cannot carry it over to the next tax year (in this case 2025/2026). You will receive a new £20,000 ISA allowance (if the amount remains the same) starting from the 6th of April 2025. We have another article where you can learn how to maximise your ISA Allowance before the ISA Deadline.

ISA Rules 2024/2025

This table shows some of the important rules regarding ISAs:

While there are many benefits to ISAs, there are some rules you should be aware of:

ISA Opening Rules

While you can use your £20,000 allowance across different types of ISAs, you may only open and contribute to 1 of each type of ISA in any given tax year. You may have 1 Cash ISA, 1 Stocks & Shares ISA, 1 LISA and 1 IFISA per tax year. In the same way, your child may only have 1 Junior Cash ISA and 1 Junior Stocks and Shares ISA per tax year.

ISA Contribution Rules (ISA Flexibility)

Once you contribute to a non-flexible ISA, that counts toward your annual limit. If you then withdraw funds, you can’t replace that money within the same tax year without using more of your allowance. In short, once it’s in, it’s in. So be sure of your choices, before contributing to any non-flexible ISA. Most ISAs are non-flexible but there are some flexible ISAs, for example flexible Cash ISAs which allow you to withdraw and re-deposit the same amount in the current tax year without forfeiting more of your allowance.

ISA Withdrawal Rules

These vary depending on the type of ISA. with a:

- Cash ISA you can withdraw anytime with an Easy Access Cash ISA, but if you choose any fixed-term account or Notice Cash ISA, then there will often be penalties for early withdrawals.

- Stocks & Shares ISA, you can withdraw anytime, but the value of your investments will depend on market conditions.

- Lifetime ISA, you can make free withdrawals for buying an eligible first home or after the age of 60. Withdrawing outside these rules, will result in a 25% penalty.

- Junior ISA, the funds are locked until the child turns 18 years old.

ISA Transfer Rules

You can transfer your existing ISAs to different providers without impacting your current year's allowance. You might wish to do this if, for example, you find better ISA savings rates elsewhere. While you can transfer between providers, you may also transfer Cash, Stocks & Shares and IFISAs to different ISA types, for example, you could transfer your Cash ISA to a Stocks & Shares ISA. LISAs and JISAs can only be transferred in full to another LISA or JISA provider, respectively. It’s important to use an official ISA transfer form in order to keep the tax-free status. Never withdraw and re-deposit your funds manually.

ISA Tax Rules

Provided you stick to the rules, your ISAs will face:

- No Income Tax – You won’t pay tax on interest accrued from a Cash ISA or dividend income from a Stocks & Shares ISA.

- No Capital Gains Tax – You won’t pay tax on the growth of your investments in a Stocks & Shares ISA.

- No Inheritance Tax – Your surviving spouse can inherit your ISAs tax free and inherit your ISAs’ tax-free status.

What are the best ISA Accounts?

You should be aware of the different types of ISA accounts available before choosing your ISAs:

Managed vs Self-Managed ISAs

In terms of management, ISAs come in 2 versions. A provider may offer one or both types:

- Self-Managed ISA (DIY ISA), where you personally pick the stocks and funds to invest your funds in, or a

- Managed ISA, where the provider picks the stocks and funds to invest your funds in (often based on your chosen risk tolerance).

Managed ISAs suit the “hands off” investor but often incurs higher fees while self-managed ISAs suit those who want to do the leg work themself while keeping fees to a minimum. Some providers offer a middle-of-the-road option with Ready-Made-Portfolios you can choose from within a DIY ISA.

Flexible vs Non-Flexible ISAs

To avoid losing out on your ISA allowance you should be aware of a further 2 types of ISA accounts, namely Flexible and Non-Flexible:

The table above shows a Flexible vs Non-Flexible ISA comparion:

- Flexible ISAs enable you to withdraw money from the ISA and redeposit it later within the same tax year without using an additional part of your ISA allowance.

- Non-flexible ISAs lack this benefit meaning that any withdrawals will permanently reduce your allowance. If you reinvest the withdrawn funds in the same tax year, this will use an additional part of your ISA allowance (as if it were a new contribution).

Therefore, if you want to withdraw and redeposit funds within the tax year, a flexible ISA will be best. If your goal is to simply invest for the long-term, then non-flexible ISAs are fine, just be certain when making any contributions.

The Best ISA for 2025/2026

This comes down to your goals and risk tolerance. This table compares all the types of ISAs and who each is best for:

In terms of specific ISA products, you can see our full comparisons linked below but here are some quick mentions.

Our comparison of Stocks and Shares ISAs found the following to be the best:

- DIY ISA for ETFs: InvestEngine Stocks and Shares ISA

- DIY ISA for US Stocks: Trading 2i2 Stocks and Shares ISA

- Managed ISA for the lowest costs: interactive investor Stocks and Shares ISA

- Managed ISA for the best performance*: Wealthify Flexible Stocks and Shares ISA

The top pick in our comparison of:

- The Best Cash ISAs was the Tembo Cash ISA

- The Best Lifetime ISAs was the Tembo Lifetime Cash ISA

- The Best Junior ISAs was the Hargreaves Lansdown Junior Stocks and Shares ISA

- Although we haven't done a full comparison, one of the best Innovative Finance ISAs is the CrowdProperty IFISA

*Performance based on our analysis which found Wealthify’s Adventurous Original Plan to have the highest annualized return over the past 5 years. Future performance may vary. Some of these are affiliate links where we might earn a commission if a user signs up.

Hopefully, you’re now ready to make the most of your ISA allowance. A reminder that the 2024/25 ISA deadline is at midnight on 5 April 2025. We hope this has helped you understand the world of tax efficient savings and investments in the UK. If you’re already a client of ours and have any questions on this, please reach out to your accountant. If you’d like to become a client, please get in touch with us today.

Remember, when you invest in stocks & shares ISAs your capital at risk. Tax treatment depends on your individual circumstances and may be subject to change in the future. The value of your investments may go down as well as up. You may not get back all the money that you invest. This communication is not intended to be a personal recommendation. If you are unsure about the suitability of an investment product or service, you should seek advice from an authorised financial advisor.

.webp)

.png)

%20(1).png)