With the ISA deadline fast approaching, now is the time to make the most of your annual ISA allowance before you lose it forever. Whether you're investing through a Stocks and Shares ISA or accruing interest through a Cash ISA, understanding the ISA limits and cut off date is essential. In this article, we explore the key dates, rules and strategies to maximise your allowance each year.

When is the ISA Deadline for 2024/2025?

The UK tax year runs from 6 April to 5 April. This means that the deadline for using your 2024/2025 ISA allowance is midnight on 5 April 2025. Since the ISA allowance works on a “use it or lose it” basis, once the ISA cut off date passes, any of your unused ISA allowance is lost forever. In short, you may not carry it over to the next ISA tax year. At the start of 6 April 2025, a new tax year (2025/2026) begins with all UK residents receiving a fresh ISA allowance. The 6th of April is, essentially, the ISA start date each year.

While midnight on 5 April is the official UK ISA deadline, some ISA providers require applications or deposits earlier than that. For example a specific provider’s ISA deposit deadline might be 5 PM or 11 PM on April 5. So, check with your provider to avoid last-minute issues.

How much is the ISA Allowance for 2024/2025?

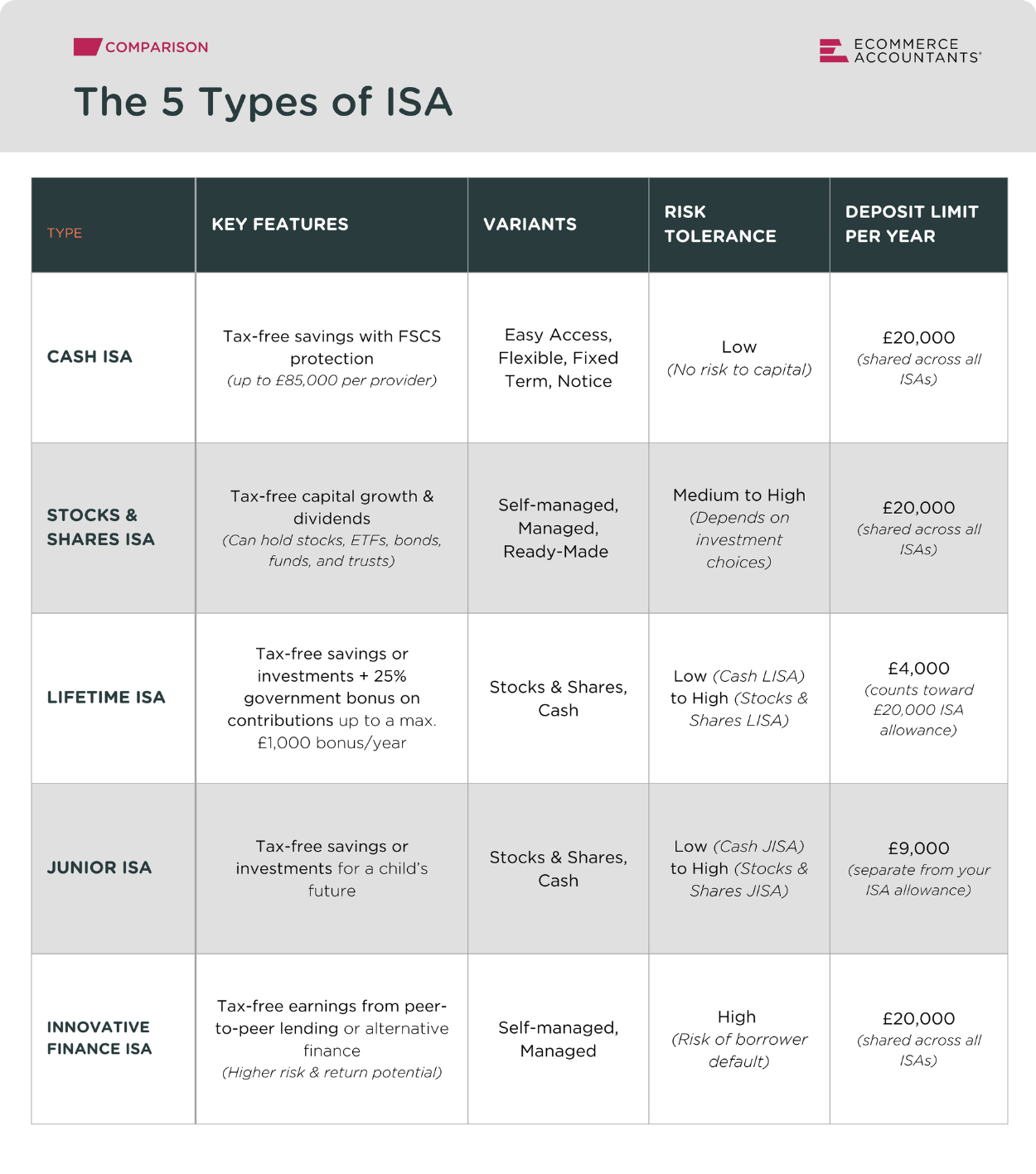

The 2024/2025 ISA allowance remains set at £20,000 per person. You may distribute this ISA limit between different types of ISAs but you may not exceed £20,000 in total across 1 or more ISAs. Here is a table showing the 5 types of ISAs and how you could spread your yearly ISA Allowance between them:

If you want to learn more, see our article covering each type of ISA and the ISA rules, but, briefly, your options include:

- Cash ISAs which you can deposit savings into and earn interest on, tax-free. There’s no specific Cash ISA allowance, so should you choose, you could deposit up to your full £20,000 into this type.

- Stocks and Shares ISAs through which you can invest in stocks, funds, ETFs and more in an effort to earn even higher returns, again, tax-free. Again, There’s no specific Stocks and shares ISA allowance, so you could deposit up to your £20,000 ISA limit into this type.

- Lifetime ISAs (LISAs) which come in the form of Cash or Stocks & Shares LISAs with the added benefit of an annual 25% government bonus on the contributions you’ve made. The Lifetime ISA allowance is £4,000 per year, meaning you could earn a maximum bonus of £1,000. This is available to those aged 18-39 with the bonus only usable for a first home purchase (at least 12 months after opening the LISA) or retirement (after age 60).

- Innovative Finance ISAs (IFISAs) which allow you to lend and earn tax-free interest via peer-to-peer lending, crowdfunding or other alternative finance models. As with a Stocks & Shares ISA, there’s no specific IFISA allowance.

- Junior ISAs (JISAs) which come in the form of Cash or Stocks & Shares JISAs, enabling you to create tax-free savings or investment accounts for children under 18. The Junior ISA allowance is £9,000 per child (across all JISA types) for the 2024/2025 tax year. This is separate to your own ISAs and does not affect your personal ISA allowance.

How to Maximise Your ISA Allowance Before the Deadline

If you haven't used up the maximum ISA allowance yet, here are some strategic ways you could utilize it before the deadline arrives:

1. Use a Lifetime ISA (LISA) if Eligible

This is number one on the list for a reason! If you're between 18-39, you can contribute a maximum of £4,000 per year into a LISA, with the government adding a 25% bonus (up to £1,000 per year). This can only be withdrawn, penalty-free, for a first home purchase or for retirement. If you’re planning for either of those, this is a magnificent way to boost those savings. Find out our top LISA pick in our comparison of the Best Lifetime ISA Accounts.

To emphasize the importance of the Lifetime ISA deadline, here is an example:

You plan to purchase your first home in a year's time and you have (or will build up) £12,000 in a savings account over this period. The home you plan to buy would be eligible under the LISA rules (purchased for up to £450,000 with a mortgage) and you know you can use your LISA funds towards the purchase after the account has been open for 12 months.

Using the deadline well:

You open a LISA and deposit £4,000 into the account before midnight on April 5 2025 and you receive a £1,000 government bonus for the 2024/25 tax year about 4 weeks later. You then deposit another £4,000 into your LISA any time between 6 April 2025 and 5 April 2026, you receive another £1,000 government bonus but for the 2025/26 tax year. On 6 April 2026, you deposit the last £4,000. In early May 2026, you receive another £1,000 government bonus, this time for the 2026/27 tax year.

In roughly 13 months, you’ve earned £3,000 in bonuses, turning your £12,000 into £15,000 (not considering any interest/growth) and you’ll be able to use the full amount towards your house purchase.

Missing the deadline:

By contrast, if you miss the deadline, even by one day, that Lifetime ISA allowance (and extra £1,000 bonus) is gone forever. To achieve the same result, you’d need to put off your house purchase for another full year to use the 2027/28 bonus.

The illustration below shows an example of how you could deposit and earn bonuses between the 2024/25 and the 2026/27 tax years:

2. Use a Cash ISA as your Emergency Fund

If you already have an emergency fund or are putting cash away each month, then why not consider transferring that into a FSCS protected, interest bearing Cash ISA? You could earn interest of up to 5%, tax-free. If you’re worried about your funds being locked away, choose an Easy Access Cash ISA where you can withdraw anytime. Even better, if you want to be able to withdraw and redeposit funds in the same tax year without affecting your tax free ISA Allowance, you can select a Flexible Cash ISA. In another article, we compare the top Cash ISAs this year.

3. Leverage the Separate Junior ISA Allowance

If you’ve already used up your personal ISA allowance, don’t forget that, as a parent or guardian, you can also contribute up to £9,000 into a Junior ISA per child per tax year. The Junior ISA Allowance is separate to your personal £20,000 ISA deposit limit. This is a great way to secure tax-free growth on investments or savings for a child’s future. We have a comparison of the top Junior ISAs this year.

4. Find the Best ISA Deals on the Market

Every ISA provider has pros and cons. Whether you’re opening new ISAs or considering switching providers, it’s worth looking at different providers to ensure you’re maximizing returns. If you’re saving, evaluate interest rates. If you’re investing, assess investment options and platform fees. To help you find the right fit, we’ve put together separate comparisons of the:

Last-Minute ISA Contributions: What To Watch Out For

As the deadline approaches, many people rush to make those last-minute contributions. If that’s you, then keep these points in mind:

- Bank Processing Times: It takes time to deposit funds into ISA accounts, particularly when there’s congestion, so aim to make those last contributions by 2 April 2025

- ISA Application and Deposit Deadlines: Different providers may have earlier cut-off times for new applications or deposits so check with yours to avoid issues (e.g. 9pm on 5 April)

- Investment Timing: If you're contributing to a Stocks and Shares ISA, consider the market before making a large, last-minute contribution

Common Mistakes to Avoid

Many savers and investors make avoidable mistakes during this time. Here are some common pitfalls:

- Waiting Too Long: This can lead to last-minute stress, poor decisions or missing the deposit window, thereby losing out on all or part of the ISA allowance.

- Exceeding the ISA Allowance: Contributions over £20,000 may not be tax-free. Remember, that’s across all ISA types, so keep track of all ISA investments each year to avoid exceeding the limit.

- Failing to Plan: There are many types of ISAs and even more providers. Take time to assess your options and apportion your Allowance across the optimal mix of ISAs to avoid overcontributing to one type or paying unnecessarily high fees

Maximizing Your Fresh ISA Allowance in 2025/26

Once the deadline on 5 April 2025 passes, the 2025/2026 tax year begins with a fresh £20,000 ISA allowance. If you failed to fully utilise your allowance in the previous year, planning early for 2025/26 will help you avoid future last-minute decisions:

1. Start Early in the Tax Year

Consider investing in your ISA/S early in the tax year. This also provides your savings or investments with more time to grow and takes advantage of compound interest.

2. Consider Transferring ISAs

Your savings or investments have a full tax year before them so you want to ensure they’re working as hard as possible for you. If you’ve found higher interest rates or favorable investment options at a different ISA provider, consider transferring your ISA to the new provider. In many cases, you can even transfer between ISA types. Just be sure to use the official ISA transfer process to retain all your tax-free benefits. Please see the rules surrounding the transfer of different ISAs in the table below.

3. Spread Contributions Throughout the Year

If you find yourself forgetting to contribute, consider setting up a monthly direct debit to slowly fill your ISA allowance over the course of the tax year. This might also be a helpful option for those who can’t face “timing the market” with a Stocks & Shares ISA.

Last Word

Be sure to calendar the ISA deadline on 5 April each year. This is a crucial date for investors looking to make the most of their ISA allowance. Start early, review your options such as those we’ve compiled on our lists of the best Stocks and Shares, Cash, Lifetime and Junior ISAs this year and, most of all, don’t let your tax-free ISA allowance go to waste. If you are a client of ours and have any questions, please reach out to your accountant. If you’re interested in becoming a client or want to learn more about our service, please get in touch with us today.

Remember, when you invest in stocks & shares ISAs your capital at risk. Tax treatment depends on your individual circumstances and may be subject to change in the future. The value of your investments may go down as well as up. You may not get back all the money that you invest. This communication is not intended to be a personal recommendation. If you are unsure about the suitability of an investment product or service, you should seek advice from an authorised financial advisor.

.webp)

.png)

%20(1).png)